Key takeaways

If you remember only one thing, make it this: Employment Allowance reduces employer NIC — not PAYE tax and not employee NIC.

- It offsets Employer Class 1 National Insurance liability as it arises through payroll.

- You must actively claim it — it is not automatic.

- Eligibility checks matter, especially for single-director-only companies and connected companies.

- If you missed it, you can often claim retrospectively for up to four previous tax years.

How much is Employment Allowance?

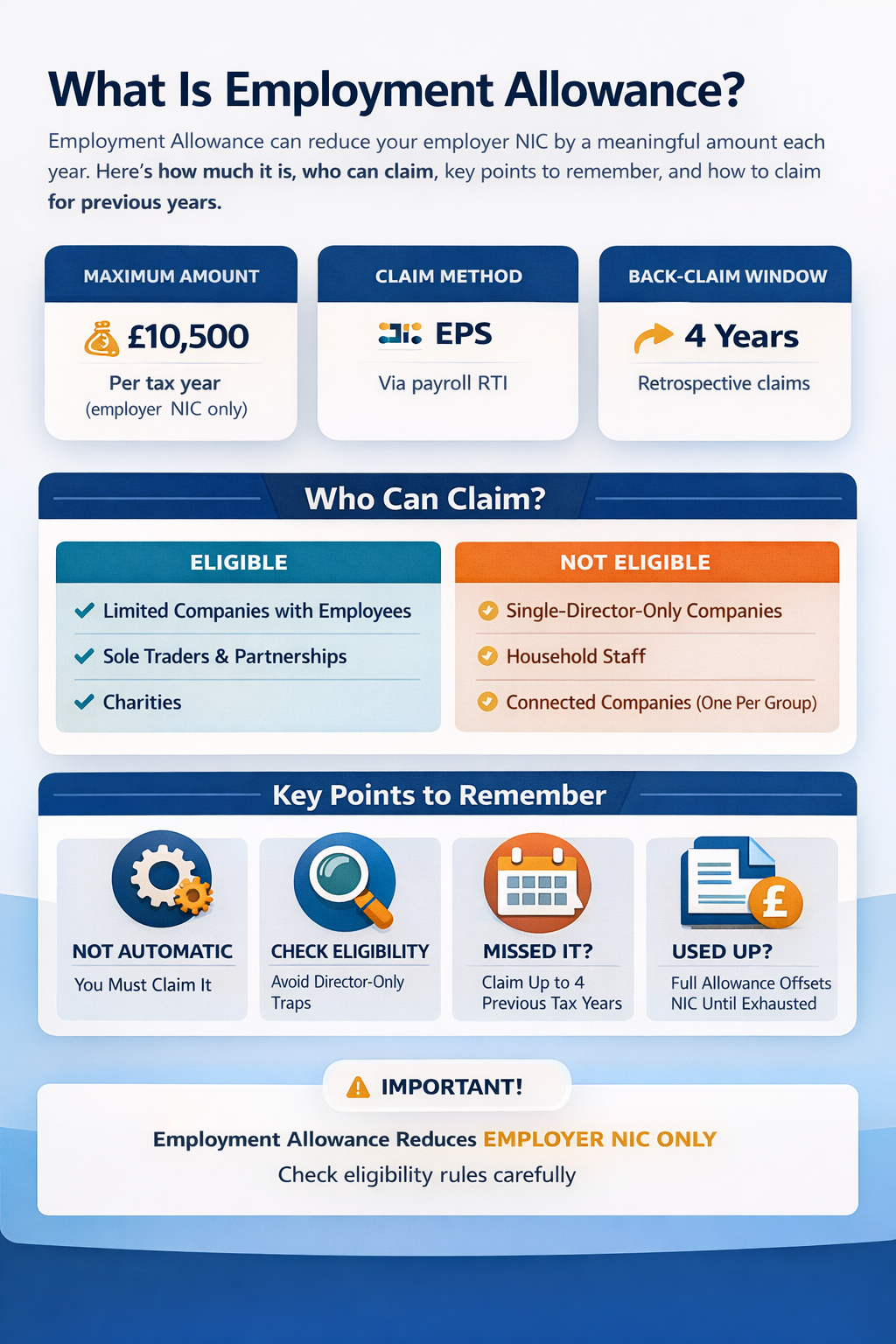

Employment Allowance currently allows eligible employers to reduce their annual employer NIC by up to £10,500 per tax year.

What it does and doesn’t do

- Employer Class 1 NIC due on payroll

- Your employer NIC element on the PAYE account (as it is offset)

- Employee NIC

- PAYE income tax

- Workplace pension contributions

The allowance is used up throughout the tax year as employer NIC arises. Once the full allowance has been used, employer NIC becomes payable again as normal. If your annual employer NIC is below £10,500, the allowance will typically reduce employer NIC to nil — but it won’t create an extra payment beyond what you owe.

Practical tip: If your payroll costs have increased recently, you may find the allowance is used up earlier in the year than expected. That can affect cashflow forecasting.

Who can claim Employment Allowance?

Most UK businesses and charities that operate PAYE and pay employer NIC can claim Employment Allowance. The key is that you must have employer NIC to offset and you must meet the eligibility rules. Eligibility is not the same for everyone.

Usually eligible

- Limited companies with employees

- Partnerships with employees

- Sole traders with employees

- Charities (subject to normal rules)

Common exclusions and traps

- Single-director-only companies with no other eligible employees

- Domestic employment (personal/household staff)

- Certain public body arrangements (limited exceptions)

- IR35 deemed payments in specific service company structures

- Connected companies: only one claim per group

Connected companies

If companies are connected (for example, under common control), only one PAYE scheme in the group can claim Employment Allowance in a tax year. The group should decide which employer will claim. This is one of the most common areas where claims go wrong.

Common mistakes that cause problems later

- Assuming the allowance is applied automatically each year

- Claiming when the business is director-only with no other eligible employees

- Multiple connected companies claiming in the same tax year

- Not re-checking eligibility after changes to structure or payroll arrangements

When did Employment Allowance start?

Employment Allowance started in the 2014/15 tax year. It was introduced to reduce the cost of employment and support smaller employers.

The allowance has increased over time. For employers reviewing historic records, remember: rules and eligibility can differ by tax year, so retrospective claims should be assessed year-by-year.

Why this matters: If you are claiming for previous years, you are not just “turning it on”. You are applying the rules that were in place at the time.

How to claim Employment Allowance for previous years

If you were eligible but did not claim Employment Allowance, you can usually claim retrospectively for up to four previous tax years. This is commonly missed when employers change software, change accountants, or assume the relief was automatic.

Practical steps

- Check payroll records for each year and confirm employer NIC existed to offset.

- Confirm eligibility for each year (including connected companies and director-only restrictions).

- Submit an amended Employer Payment Summary (EPS) for the relevant year.

- If a year is closed in software, the adjustment may need to be handled directly by HMRC.

Where a retrospective claim is accepted, HMRC may offset it against outstanding amounts due, or issue a repayment depending on your PAYE account position. The exact outcome depends on your liabilities and payment history.

Good practice: Keep a short note (internally) of why you were eligible for each year, especially where structure or ownership changed. It makes future queries easier to answer.

Final thoughts

Employment Allowance can materially reduce the cost of employment. If you are eligible, claiming it should be part of your regular payroll process — and if you suspect you missed it in earlier years, it is worth checking your records.

Disclaimer: This guide is for general information only and does not constitute tax, financial or employment advice. Rules and eligibility depend on your circumstances.