Key takeaways

If you remember only one thing, make it this: Employer NI is an additional employer cost on earnings above the secondary threshold — it is separate from employee NI and separate from PAYE income tax.

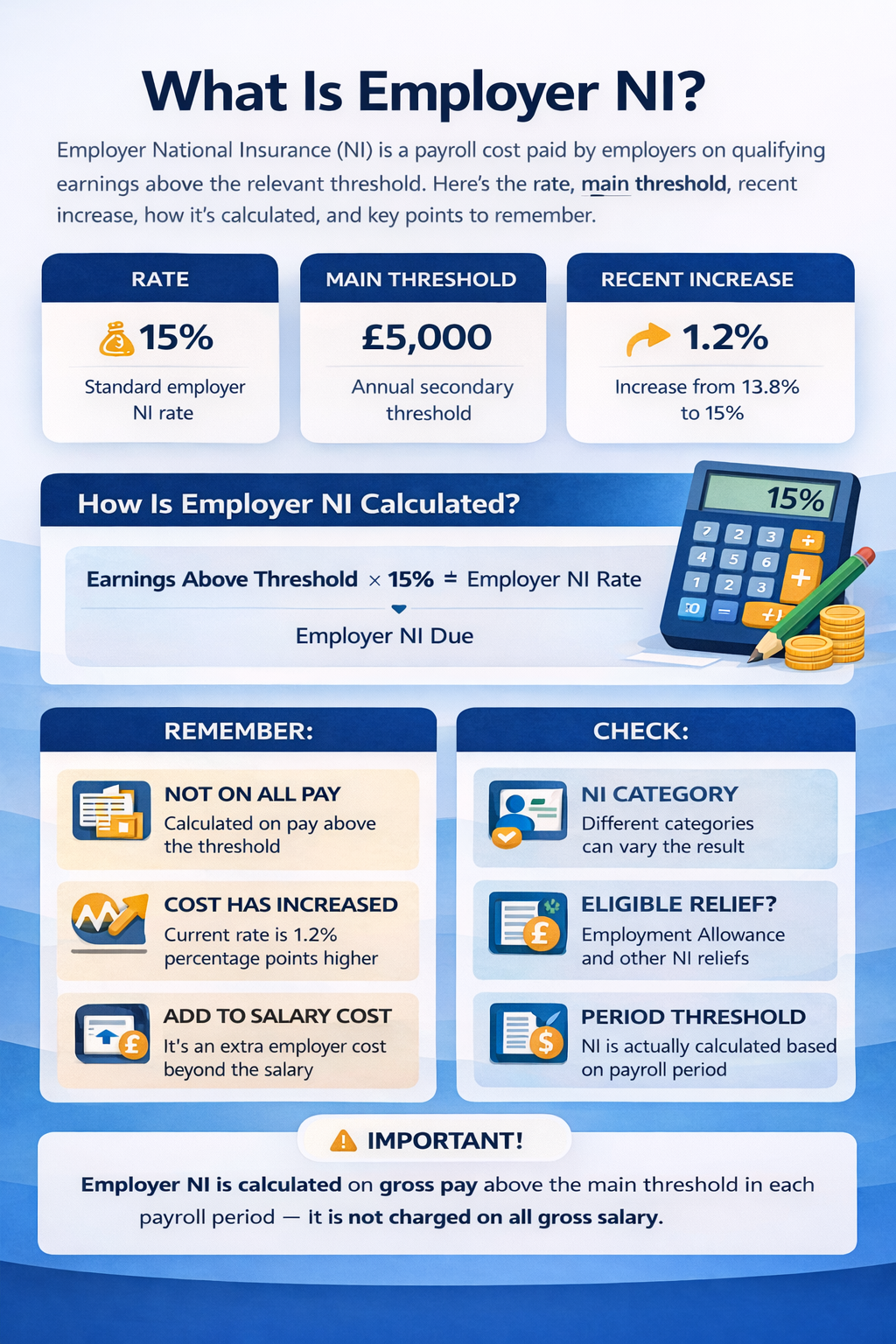

- The standard employer NI rate is currently 15%.

- It is generally charged on earnings above the employer threshold, not automatically on the whole gross salary.

- Employer NI is a business payroll cost and increases the total cost of employing staff.

- Some categories of employee can have different employer NI treatment, for example under-21s, eligible apprentices under 25, or employees over State Pension age in certain cases.

What is Employer NI?

Employer NI means Employer National Insurance contributions paid by an employer through payroll. In most standard payroll situations, it applies when an employee’s earnings exceed the secondary threshold.

It sits alongside other payroll costs such as gross pay, pension contributions and apprenticeship levy where relevant. From an employer budgeting perspective, it is one of the main reasons why the real cost of employing someone is higher than their salary alone.

In simple terms

- Employee NI from their own pay

- PAYE income tax where due

- Employer NI as an additional payroll cost

- Potential employer pension contributions

How much are Employer NI contributions?

For a standard employee under the main employer NI category, Employer NI is currently charged at 15% on qualifying earnings above the secondary threshold.

This means the exact amount depends on how much the employee earns and how often they are paid. A higher salary usually means a higher Employer NI cost, but the calculation still starts from the relevant NI threshold rather than from zero.

Practical point: When employers ask “how much is employer NI?”, the most useful answer is usually not just the rate — it is the rate plus the threshold plus the employee category.

How much has Employer NI gone up?

The main employer NI rate increased from 13.8% to 15%. That is an increase of 1.2 percentage points.

For many employers, the increase feels larger in practice because the cost is multiplied across the payroll. Even a relatively modest rate increase can make a noticeable difference once applied to several employees over a full tax year.

Why employers noticed it quickly

- It affects ongoing payroll costs every pay period

- It can materially increase the cost of pay rises and new hires

- It combines with pension contributions and other employment costs

- Higher headcount means the extra cost compounds quickly

Is Employer NI calculated on gross salary?

Not exactly. Employer NI is not usually charged on the whole gross salary from the first pound. In a standard case, it is charged on gross earnings above the secondary threshold.

So while gross salary is the starting point for understanding payroll cost, Employer NI is generally calculated only on the portion of pay that sits above the relevant employer NI threshold.

Broad rule

Gross pay determines the employee’s earnings for NI purposes, but Employer NI is usually due only on the part above the employer threshold.

Why this matters

Employers often overestimate or underestimate labour cost by applying the rate to total salary. For budgeting, quotes, recruitment planning and salary sacrifice modelling, it is better to work from earnings above threshold, not just total salary alone.

How Employer NI is calculated

In a standard payroll scenario, Employer NI is calculated by taking the employee’s NI-able earnings for the pay period, deducting the relevant secondary threshold, and then applying the employer NI rate to the balance.

Basic formula

NI-able earnings − Secondary threshold = Earnings subject to Employer NI

Earnings subject to Employer NI × Employer NI rate = Employer NI due

Example

If annual NI-able pay is £30,000 and the annual secondary threshold is £5,000, then:

- £30,000 − £5,000 = £25,000

- £25,000 × 15% = £3,750 Employer NI

Important notes

- Actual payroll uses period-based thresholds and HMRC routines

- Different NI categories can change the result

- Salary sacrifice can affect NI-able pay

- Employment Allowance may reduce what the employer actually pays to HMRC

Good practice: When estimating staff costs, look at gross salary + employer NI + employer pension. That gives a much more realistic view of total employment cost than salary alone.

What is the Employer NI rate?

The standard Employer NI rate is 15% for eligible earnings above the secondary threshold. That is the headline rate most employers are referring to when they ask about Employer National Insurance.

However, the actual amount payable can still vary depending on employee age, NI category, apprenticeship status, State Pension age, and whether Employment Allowance is available to reduce the final employer liability.

Final thoughts

Employer NI is one of the core costs of running payroll in the UK. The main point to remember is that it is usually not just “salary multiplied by a percentage” — it depends on thresholds, employee category and NI-able earnings.

For employers planning pay reviews, recruitment or overall labour cost, understanding Employer NI properly can make budgeting far more accurate.

Disclaimer: This guide is for general information only and does not constitute tax, payroll or financial advice. Employer NI depends on the tax year, employee category and payroll circumstances.